A friend living abroad recently emailed me with an observation: after five years in Europe, he's seen a noticeable shift in how the local press and social media talk about the United States. Coverage feels sharper than before. Criticism comes faster. And although he hasn't had any negative experiences personally, the broader tone feels different.

He's not imagining it. Multiple surveys confirm that international views of the United States have cooled over the past year. An Ipsos survey of 29 countries reports that perceptions of the U.S. as a positive global influence have declined in 26 of them in just six months . A wide-ranging Pew Research Center study similarly shows that favorable views of the U.S. have fallen in many nations, including major allies such as Canada, Mexico, France, Germany, and the Netherlands . Additional polling shows that in countries like Canada, France, and Germany, sizable pluralities now say the U.S. is a "negative force" on the world stage, a sharp change from only a few years ago .

While the headlines may feel sudden, the underlying dynamics follow patterns we recognize from finance, economics, and even social psychology. When you zoom out, what looks like a dramatic shift is better understood as a cycle — the same kind of sentiment cycle we see in capital markets whenever an asset, sector, or region has enjoyed a long period of dominance.

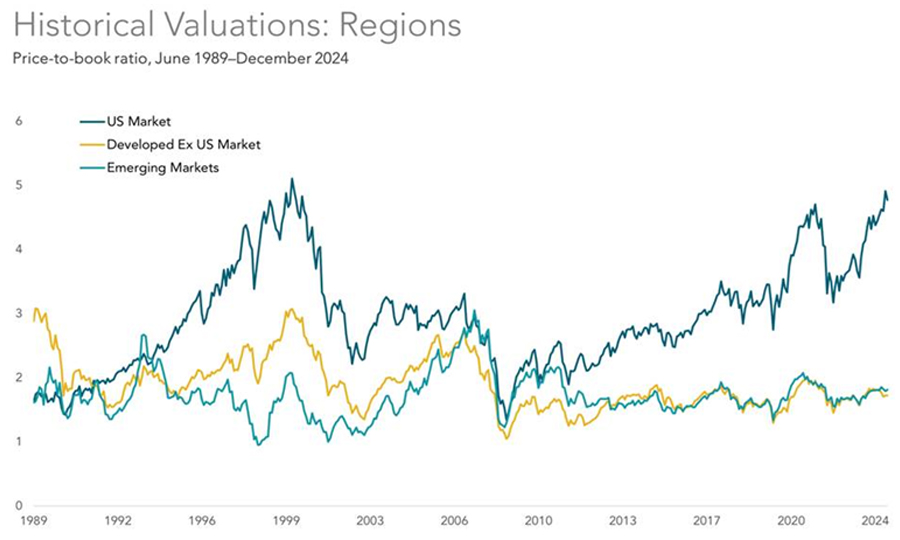

First, a chart:

I have sometimes written about finance or economics through a social, geopolitical, or psychology lens. Today I present the reverse: the current geopolitical environment viewed through a financial lens.

The Weight of Long Dominance

From a capital markets perspective, the tone shift we are seeing isn't surprising. In markets, when an asset or a sector dramatically outperforms for a long time, sentiment often reaches a point where any stumble or even just normalization triggers a reversal in mood. This is classic mean reversion. Fundamentals don't need to collapse for sentiment to swing (and in fact rarely do); it's enough that expectations became stretched. Something similar shows up in global political cycles as well.

Over the past several decades, the U.S. has led globally across multiple domains: economic scale, cultural exports, innovation, financial markets, and security architecture. In political economy research, periods like this tend to generate what's essentially a "reputational premium". But, as with a high flying stock, extended leadership eventually invites critique, hedging, and pullback. In other words, long-term outperformance leads to sentimental asymmetry.

Political science data shows that many democracies repeatedly cycle through phases of rising antiestablishment sentiment tied to inequality . These are exactly the kind of structural pressures that drive sharp, periodic swings in attitudes toward dominant global powers. A large cross country electoral database covering Europe and the OECD demonstrates that extreme or protest voting tends to rise and fall in surprisingly regular cycles, strongly correlated with inequality and austerity, globalization, and cultural identity. Similarly, the broader political economy literature highlights how global financial crises and long periods of uneven prosperity feed distrust in institutions and skepticism toward global leadership, recurring historically and across geographies. In financial terms: too much concentration in one "position" inevitably triggers rebalancing.

From Shine to Saturation

Soft power is a country's ability to attract through culture, values, and institutions. Interestingly, it is also cyclical and behaves much like an overbought asset. Early on, the world is enthusiastic, even admiring. But the longer one country sits at the center of global culture and media, the more natural it becomes for people to seek alternatives (diversification), focus on flaws (bias distortion), and simply fatigue of a saturated narrative.

Early enthusiasm leads to familiarity;

Familiarity leads to scrutiny and skepticism;

Scrutiny and skepticism lead to fatigue and distrust.

That "saturation effect" produces what looks, from afar, like a sudden shift in sentiment but it is really a return toward equilibrium. Refer back to the chart at the top of this message, and we can see that when US valuations have become extended in the past a return to equilibrium should not surprise us.

The social aspect to what we are seeing, what some have labeled a "cycle of distrust", is notable. As inequality rises and competition among elites intensifies, societies tend to move into a distrustful, zero-sum mindset. I am reminded of a recent (factually true) anecdote that in the United States as of 2025 the number of private equity firms outnumbers the number of McDonald's locations. If this is not a vivid example of how our society is becoming more unequal and dominated by "rich people transacting with other rich people, in closed loops", I don't know what is.

That mindset affects international attitudes as well. While the research doesn't speak to any one country in isolation, it does show that these distrust cycles appear across multiple countries simultaneously, which helps explain why the tone has shifted throughout Europe, not just in one region. When multiple societies enter that phase together, the global "risk appetite" for cooperation and optimism falls, much like when global markets enter a risk-off regime.

Faster Cycles, Louder Noise

In earlier eras, these shifts unfolded slowly. Today, social and traditional media technologies amplify every narrative into something sharper and more extreme than real world behavior would ever suggest. The academic literature on populism and political communication emphasizes how digital media boosts outrage, compresses sentiment cycles, and magnifies distrust signals across borders. That effect sits on top of the structural trends cited above, making the swings feel more sudden and intense than they probably are in reality. Finally, Donald Trump is a unique accelerant to this chemical reaction.

This leads to a foundational principal of good investing, one that I think has value as a social principle as well. It is the distinction we make every day in the markets: price isn't value, and sentiment isn't fundamentals. Long-term, these cycles tend to stabilize. Just as markets move through periods of exuberance and pessimism before converging back toward fair value, global sentiment toward major powers tends to oscillate and eventually normalize. Little of this signals a permanent shift in how everyday people interact or how communities treat one another.

Portfolio Design for a Changing World

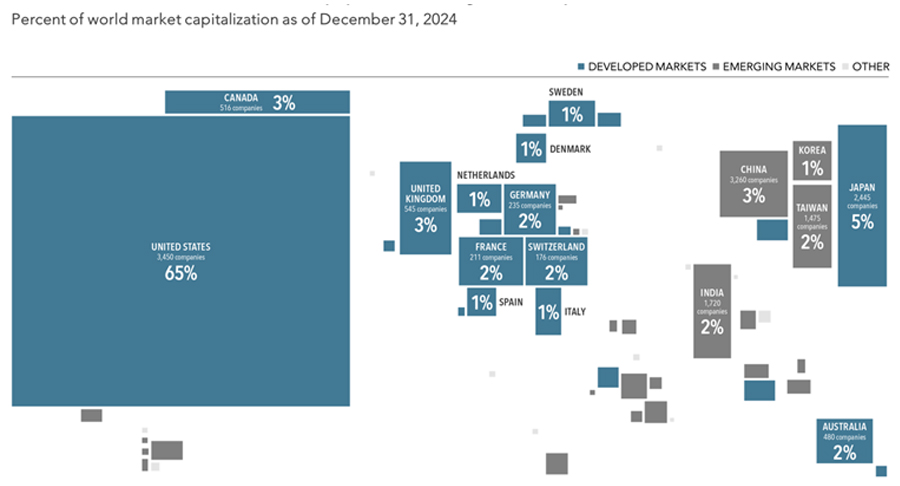

I would like to close with a comment on portfolio design, because the trend and its effects on capital markets around the world are real and do influence our clients and their financial plans. We have just seen the MSCI EAFE index (Europe, Australia and the Far East) leap by over 30% in 2025, doubling the return of the S&P500, and we have seen some of the best performances year to date come from European companies and especially defense contractors. The average American retail investor has an extreme home bias, with over 80% of their portfolio invested in US equity. A "neutral" global portfolio should be about 60% US and 40% international, but few Americans follow this. Economists attribute this extreme American home bias to a perception of safety from familiarity with companies that they interact with (such as Amazon and Visa), aversion to foreign currency risk, and historical success. In other words, home bias is typically a byproduct of sentiment and an emotionally driven style of investing.

In contrast, our portfolios have always been strongly aligned with global market capitalization, and we are currently invested at approximately 65% US and 35% international, with that modest home bias occurring because of the relatively lower cost of domestic investing. I believe that global diversification helps reduce idiosyncratic risk and positions your portfolio to capture higher returns wherever they appear. A global portfolio has a strong historical track record of outperforming a concentrated US portfolio when it comes to risk-adjusted returns over a retirement time horizon, which is the performance that is the most interesting and relevant to me, for my clients. I think that as global sentiment "reverts to the mean", this data-driven approach to investing will continue to prove its merit.

Frank Hujsa, CFP®, CLU®, CEPA®

Partner, Acadium Financial Partners

27499 Riverview Center Blvd, Suite 108

Bonita Springs, FL 34134

Any opinions are those of Frank Hujsa and are not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. The information contained in this letter does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Securities offered through Raymond James Financial Services, Inc. member FINRA/SIPC. Acadium Financial Partners is not a registered broker/dealer and is independent of Raymond James Financial Services. Investment Advisory Services offered through Raymond James Financial Services Advisors, Inc.

Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance does not guarantee future results. Keep in mind that individuals cannot invest directly in any index. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals to successfully complete CFP Board's initial and ongoing certification requirements.

Ipsos.com

Pewresearch.com

Politico.com

Dimensional Fund Advisors, used by permission. In USD. The Fama/French Indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Source: CRSP and Compustat data calculated by Dimensional. Fama/French data provided by Fama/French. US Market represented by the Fama/French Total US Market Research Index. Developed Ex US Market represented by the Fama/French International market Research Index. Emerging Markets represented by the Fama/French Emerging Markets Index. Monthly aggregate price-to-book ratios are computed as the inverse of the weighted averbook-to-marketvalue as of month-end. Firms with negative book value are excluded. Book-to-market ratios above 10 are winsorized as the cutoff value in non-US Markets.

Populist cycles: An illustrated history, The data on voting cycles and their correlates

Dimensional Fund Advisors, used by permission. In USD. Diversification neither assures a profit nor guarantees against loss in a declining market. Market cap data is free-float adjusted and meets minimum liquidity and listing requirements. Dimensional makes case-by-case determinations about the suitability of investing in each emerging market, making considerations that include local market accessibility, government stability, and property right before making investments. China A-shares that are available for foreign investors through the Hong Kong Stock Connect program are included in China. 30% foreign ownership limit and 25% inclusion factor are applied to China A-shares. Many nations not displayed. Totals may not equal 100% due to rounding. For educational purposes; should not be used as investment advice. Bloomberg data provided by Bloomberg.