What Las Vegas Can Teach Us About IPOs

My team and I were in Las Vegas recently for the Raymond James annual conference. It is an interesting place to spend time if you work in finance. There is a lot going on beneath the surface, literally and figuratively. People focus on the lights, the shows, the restaurants. But the thing that makes Las Vegas work is much simpler than that.

The games are structured in a way that produces a reliable outcome over time.

I love going to Las Vegas and typically visit several times a year. I never gamble. Not because I think gambling is wrong, but because I understand what is being offered. Every game has a design and the odds are not random; they are carefully constructed so that over time the outcome is not especially surprising.

That doesn’t mean nobody wins. People win all the time. It just means that the experience of winning and the expectation of winning are not the same thing, and the difference is what keeps the lights on and the drinks flowing.

From time to time, a similar kind of question shows up in investing. It’s not about rebalancing or taxes or whether a portfolio is properly aligned. It’s about a company that feels important. The kind of company people don’t want to miss.

Lately, that question has started to gather around SpaceX. And if it isn’t SpaceX, it will be something else soon enough. OpenAI. Anthropic. Another company that captures attention in the same way.

The question usually sounds simple: “Should we invest when it goes public?” Like most simple questions in investing, it sits on top of something more complicated.

The Crowded Table

When people picture an IPO, they often think about getting in early. Itis more like walking through a casino and noticing a crowded table. There is energy around it. People leaning in, cheering. Chips moving. It looks like something is happening there that you might want to be part of.

But the presence of a crowd does not change the structure of the game.

By the time a company reaches the public markets, a lot has already happened. Companies like SpaceX have spent years being funded, developed, and evaluated by venture capital firms, private investors, and insiders. The most uncertain and often fastest-growing phase is already behind them. When shares are offered to the public, those early participants are beginning to step back. If you enter the IPO, you are buying from them.

The opportunity is not being discovered. It is being presented.

A Strong Hand Isn’t Enough to Win the Game

IPOs often produce a burst of excitement. First-day gains of 15 to 20 percent have been common on average, and sometimes much higher in periods of strong enthusiasm.i

That initial move gets a lot of attention.What tends to get less attention is what happens next.

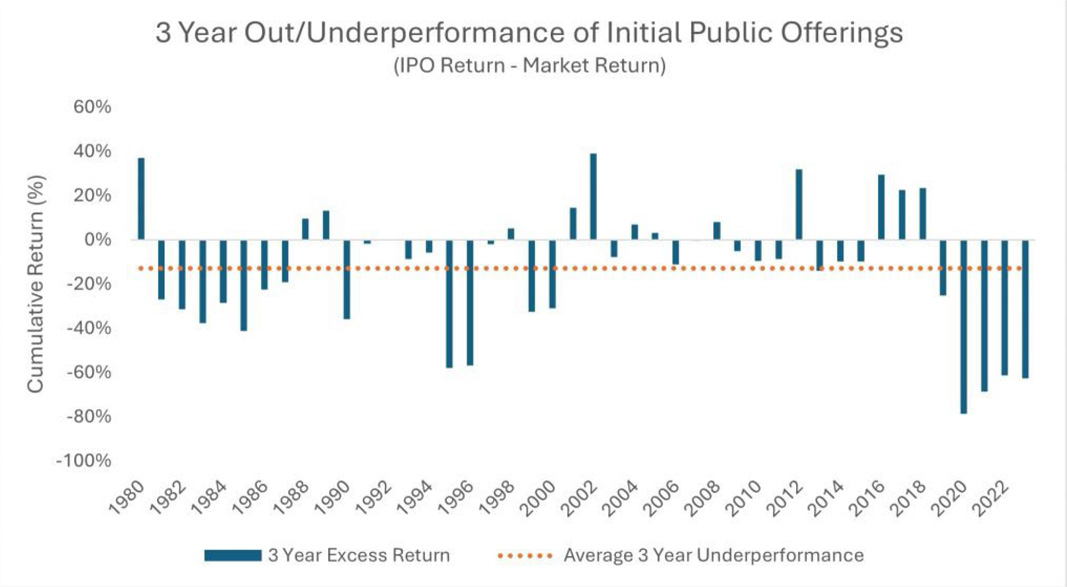

Over longer periods, IPOs as a group have tended to lag the broader market. Evidence going back decades find that newly public companies underperform similar firms in the years that follow their IPO. More recent data shows that a majority of IPOs trail major market benchmarks within a few years of going public.ii

The pattern is not subtle, and it has repeated across different market environments. The chart belowiii captures this reality. A handful of strong outcomes stand out, but most results fall short over time.

The Stories That Get Told

In Las Vegas, you tend to hear from the people who had a good night. The ones who didn’t usually keep that part to themselves.

A small number of companies go on to become exceptional long-term successes. Those are the ones we hear about most often. They are easy to identify in hindsight, but they are the exception and not the rule.

In one dataset, roughly two-thirds of IPOs underperformed the S&P 500 within three years. Some never recover. A meaningful number do not remain public over longer periods.iv

The average result reflects allthose outcomes, not just the standout successes, and this tends to become more pronounced when enthusiasm or “hype” is highest.

Periods with the most attention and the most compelling narratives often produce the most active “tables.” As Jay R Ritter finds in his paper “The Long-TermResults of Initial Public Offerings”, they also tend to produce weaker results afterward, as expectations built into the initial price are difficult to exceed.v

We saw a version of this recently with SPACs, which brought a wave of companies to market in a short period of time. Many were highly anticipated. Many delivered disappointing returns once the initial excitement faded.As in Vegas, the names and dates change but the story is often repeated.

A Different Kind of Bet

All of this points to something that is easy to lose sight of in the exciting moment. When we investlike this, we are not just evaluating a company. We are stepping into a market that has already been formed around that company, with expectations shaped by people who have been studying it for years(and who are your counterparties).

By the time shares are widely available, the question is no longer whether it is a great business. The question is whether it will be even better than everyone already believes it is. That is a very different kind of bet.

Unlike a wager in Vegas, it does not end once the decision is made. It becomes an ongoing one, whether the investor intends it or not.

What feels like a single decision is really a chain of them. Hold, sell, buy again, reassess – often as conditions change and the original story becomes less clear. As the song goes, you have to know when to hold and when to fold. Most investors never think that far ahead.

This is the real challenge: It is not enough to make one good decision. A speculative bet requires getting a sequence of decisions right, under uncertainty, without disrupting what actually produces a meaningful outcome over time: compounding.Great investors are not trying to win these moments. They are avoiding them.

The Tables You Don’t Play

Which brings us back to Las Vegas. The goal there is not to find a lucky table, it is to understand the game.

Investing is no different.

Moving from one exciting opportunity to the next means sitting down at tables where you need to be right at exactly the right time just to come out ahead. That is a difficult, costly, and stressfulway to build wealth.

Our approach is simpler.We are not trying to win these hands. We are trying to avoid games where a few bad hands can do real damage to our clients and their goals.

When others feel pressure to act, we don’t. Because we don’t speculate, we don’t depend on timing or outcomes we can’t control.

Knowing which games not to play matters more than knowing how to play them.

Frank Hujsa, CFP®, CLU®, CEPA®

Partner, Acadium Financial Partners

27499 Riverview Center Blvd, Suite 108

Bonita Springs, FL 34134

Any opinions are those of Frank Hujsa and are not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. The information contained in this letter does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Securities offered through Raymond James Financial Services, Inc. member FINRA/SIPC. Acadium Financial Partners is not a registered broker/dealer and is independent of Raymond James Financial Services. Investment Advisory Services offered through Raymond James Financial Services Advisors, Inc.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals to successfully complete CFP Board’s initial and ongoing certification requirements.

i chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://site.warrington.ufl.edu/ritter/files/The-Long-Run-Performance-ofInitial-Public-Offerings-1991-03.pdf

ii https://www.jstor.org/stable/2328687

iii https://site.warrington.ufl.edu/ritter/ipo-data/

iv https://worldmetrics.org/ipo-statistics/

v https://www.jstor.org/stable/2328